Publication

Asia M&A trends: Future outlook

Whilst global M&A rose in deal value terms in 2024, both deal values and volumes fell in most parts of Asia.

Australia | Publication | 11月 2024

On 10 October 2024, the Treasury Laws Amendment (Mergers and Acquisitions Reform) Bill 2024 (the Bill) was introduced into Parliament. The Bill is currently being considered by the Senate Economics Legislation Committee. We anticipate the Bill will be passed before the end of this calendar year.

The Bill represents the most substantial changes to competition and merger laws in Australia in some 50 years. If enacted, Australia’s existing voluntary merger control framework will be replaced with a single mandatory and suspensory administrative merger control regime, in line with the majority of jurisdictions around the world.

As currently drafted, the new merger control regime will take effect from 1 January 2026 and notification will be compulsory after that date for notifiable transactions. However, some of the transitional provisions will commence from 1 July 2025.

We provide an overview of the new merger control regime below, which supplements our previous commentary on the Exposure Draft which can be found here.

The threshold question for the new regime is whether a transaction must be notified. The notification thresholds will be set out in regulations that have not yet been released, but we provide more detail at 3 below.

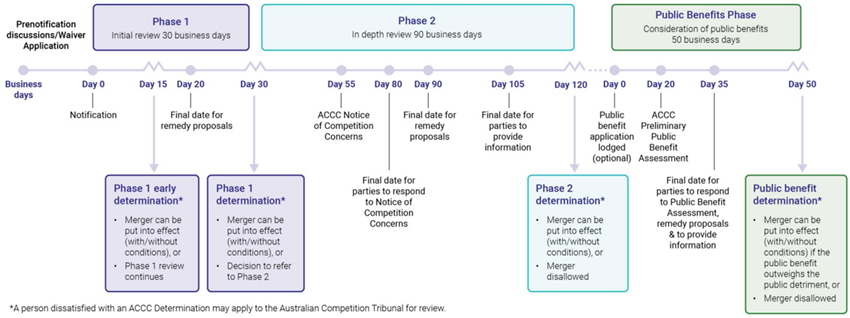

If a transaction needs to be notified, then formal notification to the Australian Competition and Consumer Commission (ACCC) must occur, unless an exemption from notification has been obtained from the ACCC. A formal statutory process then applies which sets out timelines and phases for the ACCC’s consideration of the notification.

On 10 October 2024, the ACCC issued a “Statement of Goals for Merger Reform Implementation” (Statement of Goals) which outlines its goals and objectives in delivering the Government’s merger reforms, subject to the Bill passing Parliament.

Sourced from: ACCC statement of goals for merger reform implementation

The Bill mandates that clearance decisions must be made by the ACCC within 30 business days (Phase 1) of notification, or within a further 90 business days (Phase 2) for transactions not cleared in Phase 1.

Notably, if a determination is not made by the ACCC within the statutory timeframe, subject to any allowable extensions, the acquisition will be deemed approved and can be put into effect. This will hold the ACCC accountable in meeting statutory deadlines. This is a significant shift from the current flexible timeframes for reviews in the informal regime that can be varied unilaterally by the ACCC. However, in practice we would expect the ACCC to use ‘stop the clock’ mechanisms to extend the statutory timelines, thereby providing some flexibility.

Under the proposed notification thresholds, it is likely that some transactions may be notified that do not raise any competition concerms. For these transactions, the Bill contemplates a fast-track procedure. A transaction could be cleared in as little as 15 business days after notification. The ACCC has indicated that it expects to determine around 80% of notifications in 15 to 20 business days, given that most notified transactions are unlikely to raise competition concerns.

Under the new merger control procedure, the ACCC will not be permitted to block a merger unless it has been considered in the context of a more detailed ‘Phase 2’ review. The Statement of Goals indicates the ACCC intends to enhance its use of economic and data analysis to identify risks to the community, including any risks of long-term harm to consumers which the ACCC will take into account in reaching a final determination on each merger.

The ACCC can "stop the clock" in any determination period if it issues a compulsory information request and a merger party fails to respond within 10 business days. The ACCC can also extend timeframes for any delay in responding to a voluntary request for information.

Further, if other material changes of fact occur in the notification process, the ACCC has other limited powers to suspend statutory timeframes until the changes are dealt with.

Treasury has not yet indicated what information and documents will need to be included for a notification to be considered "complete" and for the review timeline to commence. The Statement of Goals notes that the ACCC will consult with relevant stakeholders on the notification forms in early 2025. The ACCC will outline what information is required when lodging a notification and will balance the importance of informed decision making with regulatory burden.

The ACCC has stated that it intends to facilitate and encourage pre-lodgement discussions as an important step before notification occurs. Pre-lodgement discussions are intended to assist merger parties to manage uncertainty regarding notification thresholds and to also assist to resolve matters relating to information requirements. Pre-lodgement discussions are an important part of the mandatory notification regimes of overseas jurisdictions. As such, a period of engagement with the ACCC before notification will need to be factored into the transaction timelines.

We expect the aggregate effect of the merger control reforms is that it will make it easier for the ACCC to block a merger in respect of which the ACCC has concerns and more difficult for parties to challenge an ACCC decision. That being said, it remains to be seen how the new merger control regime will work in practice and the substantive legal thresholds remain largely unchanged.

Under the Bill, a threshold issue in determining whether a transaction is notifiable is whether the acquirer will gain ‘control’ of the target. Given the criticism of the broad and highly nuanced concept of ‘control’ in the Exposure Draft, it is unsurprising that the concept has been refined to align more closely with the definition of control in the Corporations Act 2001 (Cth) (Corporations Act). The definition in the Bill now relies on the capacity to influence or determine the financial and operating policies of a body corporate, and a person will be taken to control a body corporate if they or their associates jointly have this capacity. This also brings the regime largely in line with its international peers.

A ‘safe harbour’ provision has also been introduced, so that acquisitions of interests in listed, or unlisted but widely held, companies that do not result in the acquirer holding more than 20% of the voting power, will not need to be notified. This is also broadly consistent with the position in the Corporations Act.

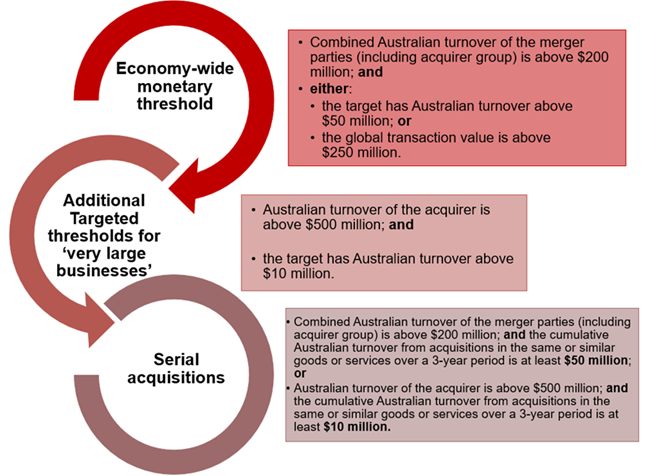

The Bill does not set out the financial thresholds above which an acquisition will need to be notified to the ACCC. Instead, these will be determined by the Minister by regulation, thereby providing the Minister with significant flexibility to refine the merger notification thresholds over time. Although the regulations are not yet available, the Government has started consulting on the notification thresholds and released a detailed consultation paper in August 2024.

In his press release of 10 October 2024 (Press Release) and the Second Reading Speech, Treasurer Dr Jim Chalmers broadly indicated the notification thresholds that will be implemented under the new regime. According to the Press Release and Second Reading Speech, there will be three key thresholds as follows:

The regulations will clarify how turnover and transaction value are calculated for the purposes of meeting the monetary thresholds.

The following diagram captures these economy-wide thresholds:

At this stage, it appears the Government has decided to not proceed with the market share concentration-based notification thresholds which featured in the Exposure Draft in the form of economy-wide thresholds. This is to be commended, as market share thresholds are inconsistent with international best practice, and their removal reduces the complexity of the proposed thresholds while providing clarity around which acquisitions are notifiable.

The thresholds will be reviewed 12 months after coming into effect, to ensure they are operating as intended.

In response to industry feedback, the Bill also introduces a waiver process. This allows merger parties to request the ACCC provide an exemption from notification requirements in relation to an acquisition. This would be used for transactions that are technically caught by the thresholds but clearly raise minimal competition issues. At this stage, the details of this process remain unclear. Further information is needed around the ACCC’s discretion and the application process to assess whether the process will operate effectively. It will be important to get the balance right to reduce burden on both business and the ACCC.

The Bill excludes land acquisitions related to residential property development and certain commercial properties from notification requirements, unless specific criteria are met (see supermarkets below). This aims to streamline the process and avoid unnecessary system congestion for those industries.

The Bill also gives the Treasurer broad powers to determine different thresholds for particular industries, types of assets or specific parties. The Treasurer has already stated that “the government intends to make sure the ACCC is notified of every merger in the supermarket sector”, and that “the government will also consider designation requirements for sectors such as fuel, liquor and oncology radiology”. It is currently unclear what thresholds could be applied for these sectors, so we will need to wait for further details once the regulations are released.

Under the Bill, in order to block a transaction, the ACCC must be ‘satisfied’ that the notified acquisition, if put into effect, would, in all the circumstances, have the effect, or be likely to have the effect, of substantially lessening competition in any market (SLC test). This differs from the Exposure Draft, whereby the ACCC was unable to prevent an acquisition unless it had a reasonable belief that there was a real possibility that the acquisition would have the effect of substantially lessening competition. The ‘satisfied’ test which is included in the Bill aligns more closely with the decision-making process of other administrative bodies.

The SLC test is one of the central concepts used in the Competition and Consumer Act 2010 (Cth) (CCA). The Bill has expanded the definition of SLC to include ‘creating, strengthening or entrenching a substantial degree of power in a market’, but only in relation to the merger control provisions of the CCA (rather than the whole CCA, as proposed in the Exposure Draft). The Explanatory Memorandum to the Bill (Explanatory Memorandum) notes that the “amendments emphasise the importance of considering the competitive structure of the market in the overall assessment of the effects of the acquisition on competition, by making it clear that a substantial lessening of competition can include creating, strengthening or entrenching a substantial degree of market power.”

The Bill also targets serial or “creeping” acquisitions, by enabling the ACCC to look at the combined effect of all acquisitions put into effect in the 3 years before the notification date where these include any party (or related body corporate of a party) to the notified acquisition and the targets of which are involved (directly or indirectly) in the supply or acquisition of the same (or substitutable or competitive) goods or services, disregarding geography. This concept is novel to Australian competition law and there remains some uncertainty as to how this new cumulative effect will be assessed in practice.

If the ACCC has made a determination that a proposed acquisition has failed the SLC test and hence should be blocked, the notifying party may then apply to the ACCC for a determination that the acquisition would be of public benefit and should be approved on this basis. In such circumstances, in order to approve the transaction, the ACCC must be satisfied that, where the acquisition is to be put into effect, the acquisition would, in all the circumstances, result, or be likely to result, in a benefit to a public. Moreover, that benefit would, in all the circumstances, outweigh the detriment to the public that would result, or be likely to result, from the acquisition.

The Bill does not contain the higher threshold of “substantial benefit” which was included in the Exposure Draft, hence the public benefit application more closely aligns with the existing merger authorisation procedure currently set out in the CCA.

A novel feature of the new merger control regime is that the ACCC will have the ability to invalidate certain restraints in M&A documentation irrespective of whether it ultimately provides a clearance for the transaction.

Currently, provisions in business sale contracts that are solely to protect the goodwill of a business for the purchaser are exempt from the prohibitions against anticompetitive conduct in Part IV of the CCA. The ACCC will be able to declare that this goodwill exemption does not apply, for example, where the contract includes a non-compete clause, and if the duration and/or geographic scope is broader than necessary for the protection of the purchaser in respect of the goodwill of the business.

The broader the scope or longer the duration of a restraint, the less likely any restrictions on the activities of the parties will be regarded as necessary and solely to protect the goodwill of the business. As such, parties need to consider whether any non-compete clauses and other provisions intended to restrain the vendor for the benefit of the purchaser are necessary and whether they may be invalidated by the ACCC.

Under the Bill, the Australian Competition Tribunal (Tribunal) will replace the Federal Court of Australia as the primary review body for mergers. Merger parties and third parties with a "sufficient interest" will be able to apply to the Tribunal for a merits review of the ACCC’s merger decisions, provided they have reasonable prospects of success.

Importantly, an appeal to the Tribunal is therefore not limited to the merger parties. The Tribunal will have discretion to allow other persons to seek a review of a determination, having regard to:

It will remain to be seen whether a party seeking to ‘spoil’ a merger would be permitted by the Tribunal to appeal a decision by the ACCC to approve a merger, although we assume this would be highly unlikely in practice.

As part of the merits review, the Tribunal may have regard to any information, documents or evidence given to the ACCC in connection with the determination, excluding information, documents or evidence to which the ACCC was not permitted to have regard in making the determination (s 110R). In a welcome change, the Tribunal will also have discretion to review new documents and information from merger parties which were relevant to the grounds upon which the ACCC made a determination, where the merger parties did not have a reasonable opportunity to make submissions to the ACCC on those grounds. The Bill also allows for technical experts to be called and cross-examined in reviews of acquisitions. The change of review body may thus impact merger outcomes, due to differing evidentiary and procedural rules between the Federal Court and the Tribunal.

One of the key goals of the merger reform is to make Australia’s merger control regime more transparent. To that end, the Bill provides that the ACCC must publish a public register of all mergers that have been notified to the ACCC. The Statement of Goals clarifies that the ACCC will publish its findings on the acquisition notification process, any Notices of Competition Concerns provided to merger parties in Phase 2, and provide reasons for its decisions, including for final determinations and decisions to refer a deal to Phase 2.

A key point of concern arising from the Exposure Draft was the extent to which such transparency would be applied. Importantly, publishing notifications on the public register represents a significant change from the current situation, where the vast majority of merger reviews by the ACCC are conducted on a confidential basis and are not reported to the general public. It will also provide interested third parties with a greater ability to comment on proposed transactions and raise potential concerns.

Following consultation on the Exposure Draft, the Bill includes a new process that will enable surprise/hostile on-market takeovers of publicly listed companies to be confidentially reviewed by the ACCC and then listed on the public register after a period of 17 business days. If the ACCC makes a determination on such a takeover before the 17th business day, then information or documents relating to the takeover will not be published on the registry at all.

The Bill contains extended transitional periods for the new merger control regime, by proposing 1 July 2025 as the date when a party can notify the ACCC under the new regime. This extended period is to be welcomed by providing more flexibility for transactions likely to raise competition concerns that could involve an ACCC decision-making process extending into 2026. However, it will place the ACCC under significant pressure to implement all necessary guidelines in the first half of 2025.

If a merger is likely to be notifiable under the new regime and involve an ACCC decision date that could fall in 2026, we anticipate that merger parties would consider notifying the ACCC under the new regime from 1 July 2025 rather than seeking voluntary informal clearance under the current regime. At this point, it is unclear how the ACCC will transition any informal reviews that are still ongoing when the new regime commences in full in 2026, and we will find out more when it releases its updated merger guidelines.

For the next few months, it’s business as usual. The legislation will need to be enacted into law and the underlying regulations promulgated so that the notification thresholds are set. Once this occurs, parties will be able to start assessing whether the acquisition will be notifiable.

If an acquisition is notifiable, the next consideration would be whether completion would occur before the new regime commences on 1 January 2026 and whether ACCC informal clearance would be required. Complications may arise for those notifiable transactions with completion dates that could extend into 2026 or if ACCC approvals are required with timelines that could extend into 2026. In such circumstances, careful thought on merger strategy will be required.

However, one important immediate matter to be aware of is that businesses pursuing a roll-up strategy or an ongoing program of smaller acquisitions may already be within the 3 year look-back period that will be facilitated by the new merger control regime. As such, acquisitions made now may count in the context of notification thresholds for acquisitions made after 2026, and the ACCC could consider the cumulative effect of any such acquisitions in the context of acquisitions later notified to it.

Additional important detail will be released in coming months. We expect that the proposed notification thresholds will be formally published in the regulations, and that the ACCC will provide further details about the information that merger parties must lodge and how the waiver process will work, and will consult on new Merger Guidelines (likely reflecting developments in the United States and Europe). We will keep you updated.

Under the new regime, the ACCC will play a significantly more active administrative role than its current position. The Government’s merger reform will have an economy-wide impact. It is important for businesses to review the proposed changes to the regime and consider how they may be affected.

Please reach out to the Competition team at Norton Rose Fulbright if you would like to discuss any aspects of the Bill or the impact the merger reforms could have on your business.

Publication

Whilst global M&A rose in deal value terms in 2024, both deal values and volumes fell in most parts of Asia.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2025