Publication

Insurance regulation in Asia Pacific

Ten things to know about insurance regulation in 19 countries.

Global | Publication | décembre 2020

You can read more stories like this by subscribing to our monthly Energy Transition newsletter here.

At the start of the year, the appetite for clean energy was already evident in the Middle East. In January 2020, Bloomberg New Energy Finance predicted solar and wind would “push the region’s electricity mix to 39pc zero-carbon by 2050”.

Similarly, the HSBC Sustainable Finance and Investing Survey issued in September 2019 had predicted 85pc of issuers and investors in the Middle East to reallocate capital towards green financing goals by 2025.

The energy transition drive had also been emphasised by one of the region’s largest economies, Saudi Arabia, which announced its Vision 2030 plans in 2019. These plans include the development and installation of 58.7GW of renewable power sources (amounting to 30pc of the kingdom’s power mix) and to cut down on 130mn t of CO2 by 2030.

In the UAE, Dubai Electricity & Water Authority (Dewa) announced that it had surpassed its 2006 targets of 7pc of the total installed electricity capacity in Dubai being derived from clean energy sources by 2020, showing that it was well on its way to achieving its ambitious target of 50pc clean energy generation by 2050.

By November 2020, the positive appetite for clean energy among the hydrocarbon-dependent economies of the Middle East had transitioned into a critical yet second-in-priority need to diversify energy mixes, with state-owned enterprises focussing their attention on public spending programmes such as healthcare and other more urgent remedial packages to overcome the pandemic.

The decline in the region’s energy use due to local government lockdown measures has not been sufficient to offset the fall in oil and gas export revenues, which the IMF estimates to be around $230bn.

The Middle East has seen continued investment in new renewable energy projects in recent months.

In Middle Eastern states where oil production costs are lower and foreign exchange reserves are higher, such as Saudi Arabia and the UAE, the effects of the pandemic are likely to be better managed; where oil production costs are higher and foreign exchange reserves and sovereign wealth fund savings are lower, there is a genuine threat of an economic crisis.

Nevertheless, the Middle East has seen continued investment in new renewable energy projects in recent months.

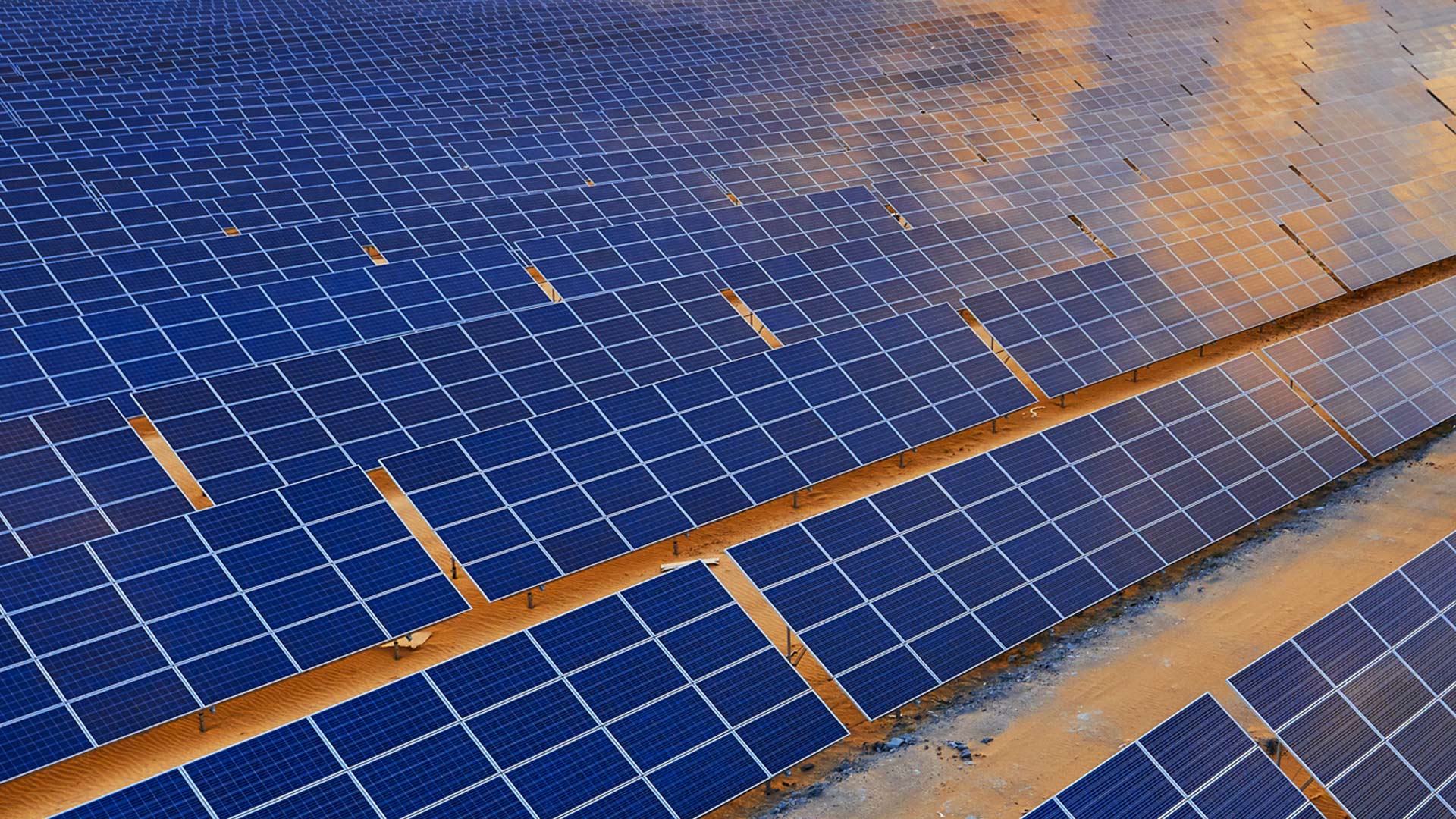

The UAE has established itself as a key solar market over the past few years, and investment continues in this space, with a number of projects ongoing or recently closed. In Dubai, the 900MW solar PV fifth phase of the Mohammed bin Rashid Al Maktoum Solar Park recently reached financial close. In Abu Dhabi, financial close is imminent on the 2GW solar PV project—forming the largest solar PV plant in the world— in Al Dhafra region.

Adnoc on 12 November signed a framework agreement with Total for a joint R&D partnership to discover opportunities for renewable energy operations and carbon, capture, utilisation and storage (CCUS) with the aim of reducing CO2 emissions. Through this partnership, Adnoc has also announced plans to expand the capacity of its Al-Reyadah CCUS facility by six times, which would capture 5mn t of CO2 from its gas plants by 2030.

In Oman, the 500MW Ibri 2 solar PV independent power project (IPP) achieved financial close and the tenders for two 600MW solar schemes in Manah have begun, facilitating the country’s plans for renewable energy to account for 16pc of the generation of electricity by 2025.

$230bn – Fall in oil and gas revenue during pandemic.

In late September, Jordan announced a new national strategy to reduce its gas imports, which account for 95pc of its domestic gas supply, by increasing its renewable energy capacity over the next five years by 37.5pc. The government is focussing on grid capacity before introducing new projects, which it hopes will match the scale of ongoing projects such as the 200MW Baynouna solar PV scheme.

Saudi Arabia, under its National Renewable Energy Programme (NREP), has been undergoing a tendering process for six solar PV IPPs since April. These include the 300MW Jeddah solar PV, 300MW Rabigh solar PV, 200MW Qurayyat solar PV, 600MW Al-Faisaliah PV, 50MW Medina solar PV and 20MW Rafha solar PV. The kingdom’s energy ministry revealed the successful bidders will enter into a 25-year power-purchase agreement with Saudi Power Procurement Company as the offtaker; execution of these PPAs is expected by year-end. These projects are part of the NREP’s clean energy targets, which include the generation of 27.3GW of renewable energy by 2024 and 58.7GW by 2030.

The Middle East has also seen a number of new water and sanitation projects. Given that one of the key challenges the region is facing is that of water scarcity, there remains a real need for regional governments to invest heavily in water, with the involvement of the private sector.

In Dubai, it is expected that Dewa and the selected developer team will be imminently signing the water purchase agreement for the emirate’s first independent water project in Hassyan. The Hassyan project is part of the UAE’s Dubai Clean Energy Strategy 2050, which aims to produce 100pc of desalinated water from waste heat and clean energy.

This follows off the back of the Taweelah RO IWP, which is in its construction phase—the first desalination project to receive a ‘sustainable loan’ qualification globally. The project incorporates a 70MW PV plant to complement energy supply from the electricity grid; this is a trend that we expect to see going forwards given the energy-intensive nature of desalination processes and the region’s drive towards sustainable development.

In Saudi Arabia, in line with the kingdom’s 2030 vision, the government has committed to develop desalination capacity and improve wastewater treatment capacity in the country. In Saudi Arabia alone, there are 23 new projects planned over the next seven years—12 desalination projects and 11 wastewater treatment projects.

Given the region’s abundant renewable energy resources, availability of investment capital, land mass and infrastructure, the Gulf states are in prime position to take the reins in the green hydrogen market, which remains in its infancy but which is very much projected to be a growth area for the region. There are clear signs from the past two years that, despite the lack of regulatory framework for the licensing and implementation of such projects, CO2-free hydrogen is of particular interest to policymakers in the region.

Earlier this year, the UAE environment minister was quoted as saying “hydrogen produced by renewables in the very best locations in the UAE could become cost competitive in the next five years”.

By 2050, the strategy consulting arm of PwC, Strategy&, claims the market could be worth $300bn/yr. With the cost of green hydrogen having already fallen by 50pc since 2015 and with a further 30pc reduction on the cards by 2025 according to IHS Markit, opportunities for states with large renewables capacities, such as the Gulf states, will be plentiful.

In the Middle East, Covid-19 has refocused regional priorities on sustainable development.

In July, Saudi Arabia’s Neom smart city agreed with US company Air Products and the Saudi power and desalination utility, Acwa Power, to create the largest hydrogen project in the world, worth $5bn. A combined renewable power capacity of 4GW, derived from wind and solar, will power the production facility. With the kingdom being home to one of the world’s cheapest solar projects, the 300MW Sakaka, the Neom project has the potential to produce hydrogen at record low prices.

The green hydrogen market is projected to grow rapidly in the coming years, with many key players in the energy sector identifying the developments in green hydrogen as important accelerators for energy transition and enabling a wider global decarbonisation.

The ramifications of Covid-19 have added impetus to the global energy transition. Since Q2 of 2020, fossil fuel consumption and CO2 emission levels have plummeted and renewable energy has re-emerged at the forefront of discourse. Businesses have been subject to and will continue to face mounting pressure from the public, regulators, industry experts, organisations and governments to focus more heavily on ESG policies in the battle towards normalcy.

In the Middle East, Covid-19 has refocused regional priorities on sustainable development. With demand for energy continuing to rise in the region and increasing pressure from governments, investors and consumers to support the decarbonisation of the industry, energy transition is set to remain at the forefront of regional governments’ priorities.

Publication

Ten things to know about insurance regulation in 19 countries.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2025