Publication

International arbitration report

In this edition, we focused on the Shanghai International Economic and Trade Arbitration Commission’s (SHIAC) new arbitration rules, which take effect January 1, 2024.

Global | Publication | abril 2024

The insurance industry is founded on predicting, as accurately as possible, whether or not a risk will materialize in a fast-moving competitive environment. Such predictions are intensively focused on data.

AI promises new insights by analyzing more data points, simultaneously across multiple data sets, leading to automation of complex cognitive processes. However, this comes with risks. Without regulation, AI models can replicate and reinforce bias of the past, with no regard for current social constraints or indeed long-term social cohesion.

For governments to achieve the benefits of AI adoption they need to ensure that society trusts in such AI, through safeguards in design, operation and management of the models, as well as accountability for AI operators when things go wrong.

However, where regulatory approaches diverge across jurisdictions, in practice, international businesses may be forced to respond to the highest standards, regardless of the differing levels of country-specific intervention.

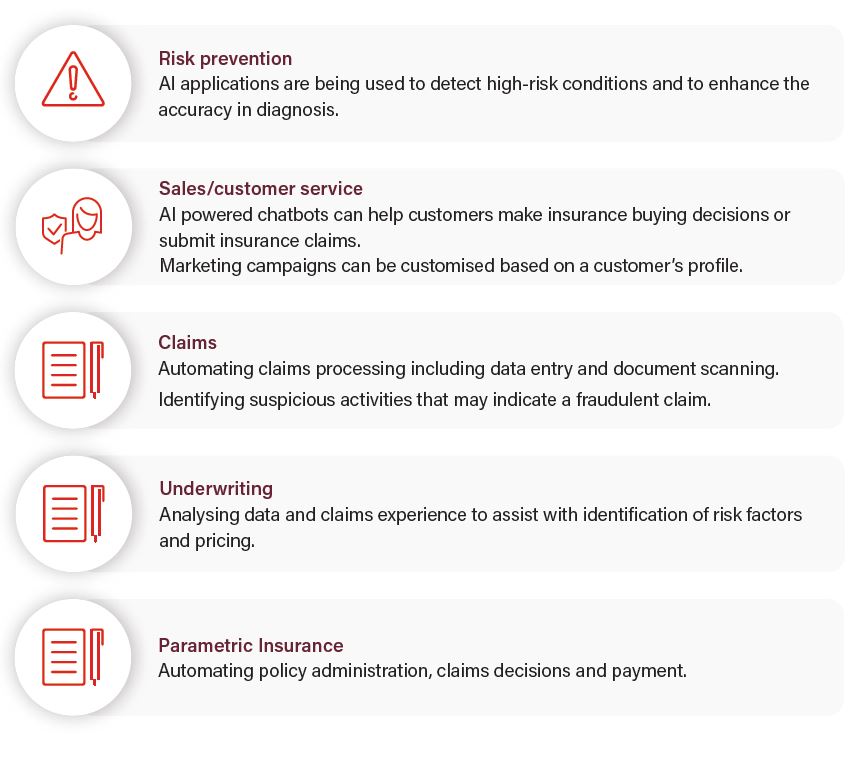

AI is transforming the insurance industry by enabling automation of repetitive tasks and generating insights from large data sets. Some applications by insurers include:

Given the wide range of use cases in which AI can be deployed, governments across the world have sought to articulate clear rules to guide those developing or deploying AI. This piece briefly summarizes the current regulatory state of play in the insurance sector in the EU, Germany, UK, Singapore, US, and Australia.

Publication

In this edition, we focused on the Shanghai International Economic and Trade Arbitration Commission’s (SHIAC) new arbitration rules, which take effect January 1, 2024.

Publication

On September 18, 2024, the "Decree amending the list that sets forth goods whose import and export are subject to regulation by the Ministry of Energy" (the "Decree") was published in the Federal Official Gazette.

Publication

On September 18, 2024, the "Decree amending the list that sets forth goods whose import and export are subject to regulation by the Ministry of Energy" (the "Decree") was published in the Federal Official Gazette.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2025