Introduction

DAC 6 imposes mandatory reporting of cross-border arrangements affecting at least one EU member state where the

arrangements fall within one of a number of “hallmarks”. The use of broad categories designed to encompass particular

characteristics viewed as indicative of aggressive tax planning follows the approach taken by the UK in implementing its DOTAS

regime back in 2004. The hallmarks under DAC 6 are much broader, however, and more parties are likely to find themselves

being classed as “intermediaries”, on whom the reporting obligation falls, than is the case with those classed as “promoter” under

the DOTAS regime. The potential application of DAC 6 to standard transactions with no particular tax motive creates a difficult

compliance burden.

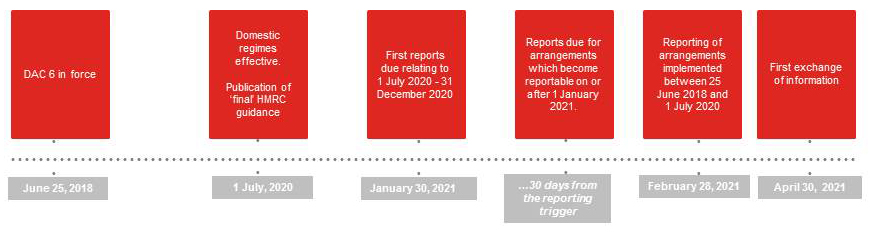

Difficulties have been compounded by the implementation timeline, which provides for implementation with retrospective effect,

meaning that the disclosure obligations were “live” from June 25, 2018, before any implementing legislation or guidance had

been published.

Reporting was intially expected to start in Summer 2020 but, responding to the challenges presented by the COVID-19 pandemic,

the EU introduced an optional six-month delay to reporting deadlines. The UK (and all member states other than Germany, Austria

and Finland) implemented this deferral.

The UK implemented DAC 6 via the International Tax

Enforcement (Disclosable Arrangements) Regulations in

January 2020 with effect from July 1, 2020. The Regulations

largely imported the drafting and definitions of the Directive so

did not provide much additional clarity. HMRC published final

guidance at the start of Summer 2020 and it is this guidance

that provides some helpful steers on how HMRC will approach

DAC 6.

The cross-border implementation of the regime adds to the

compliance burden as the reporting position may need to

be reviewed in more than one EU jurisdiction to ensure the

domestic rules are aligned. This means that if a conclusion is

reached that reporting is not required in the UK on the basis

of HMRC guidance, it cannot be assumed that the same

conclusion will be reached in other Member States involved;

something which seems contrary to the aim of having an

EU-wide reporting regime.

The headlines

- HMRC split intermediaries into “promoters” (similar to the

DOTAS concept) and “service providers” (those not directly

involved in structuring or promoting an arrangement).

Service providers only have a reporting obligation if they

know or could reasonably be expected to know that they

are involved in a reportable arrangement. The guidance

provides some reassuring commentary on what will be

deemed to be in the knowledge of an intermediary acting as

a service provider.

- A number of the hallmarks only apply where a “main

benefit” test is met and the guidance provides some

useful clarification of this test. The test is to be applied

objectively, looking at the benefits a person might

reasonably be expected to obtain, rather than actual motives

and objectives. There will be no “tax advantage” if the

consequences of the arrangement are in line with the policy

intent of the legislation the arrangement relies on. On this

basis, HMRC view products such as ISAs and pensions

or claims for R&D relief as not caught unless by reason of

being part of a wider arrangement.

- Many hallmarks are open to extremely broad interpretation

and the guidance provides some helpful examples in areas

such as cross-border transfers and income into capital

conversion. It is unclear how far that guidance can be read

across to arrangements with largely analogous features.

- Whilst HMRC’s interpretation potentially limits the extent

of UK disclosure in several areas, including standardised

products and double depreciation, where other jurisdictions

take a different approach this may, of course, not limit

reporting requirements in practice.

- Reporting will be online and HMRC will allocate an

“arrangement reference number” (ARN) to the reported

arrangement. Relevant taxpayers will then have to include

this ARN in their income or corporation tax return referred

to as making an “annual report”) for each subsequent

period in which they obtain a tax advantage as a result

of the arrangement.

- The default penalty for failure to report is £5,000 but if

HMRC consider this too low (perhaps due to deliberate

or repeated failure), the First-tier tribunal can impose daily

penalties of up to £600 or, if it considers that is too low,

has discretion to impose penalties of up to £1m. Penalties

for failure by a relevant taxpayer to make an annual return

can be up to £5,000 for the first failure within three years,

rising to £10,000 per arrangement for a third or subsequent

failures.

- No penalty will be due if there is a “reasonable excuse” for

failure to comply. The guidance stresses the importance

of having “reasonable procedures” in place to ensure

compliance when considering whether a person has a

“reasonable excuse” for a failure and casts some light on

what those procedures might involve. More generally, steps

taken to comply will be taken into account when considering

the level of any penalty even where the “reasonable excuse”

defence is not available.

How far does HMRC’s guidance take us?

It has been clear, since the publication of the Directive in

June 2018, that the DAC 6 reporting obligations would be

far-reaching and that they would impose a significant

compliance burden. What is evident now that DAC 6 has been

implemented by Member States is just how problematic the

cross-border nature of the regime is and that it may give rise to

surprising results.

In a number of areas where concerns had been raised during

formal and informal consultation, such as the reporting of

standardised products, double depreciation of an asset or

cross-border transfers, HMRC are proposing to adopt an

interpretation which seeks to limits the potential extent

of disclosure. HMRC’s guidance also provides reassuring

comments in relation to the extent of an intermediary’s deemed

knowledge of the arrangements.

Unless the approaches taken by tax authorities in respect of

their domestic regimes are aligned, however, this will not affect

whether disclosure is required in another member state. UK resident

intermediaries concluding that there is no reporting

requirement in the UK may well need to consider the rules in

a number of other relevant jurisdictions and make reports in

jurisdictions with which they have more limited involvement,

adding a significant compliance burden.

Where a report needs to be made and exactly what needs

to be reported is far from straightforward. A London branch

of an international bank headquartered in another member

state is likely to need to report London-arranged transactions

in its head office jurisdiction, rather than in the UK. If the

arrangement is not reportable in that jurisdiction because of the

way that jurisdiction has implemented the Directive, the bank

may need to consider the position in the UK (branch location).

The London branch may also be surprised to hear that HMRC

do not consider the fact that an arrangement is compliant with

the Banking Code of Practice as meaning that it is outside DAC

6. The reporting position of branches of entities headquartered

in third states is not consistent across member states. It is a far

from straightforward regime to comply with.

The UK guidance: Who is an intermediary?

Intermediaries have the primary obligation to report. The

draft regulations define “intermediary” by reference to the

Directive. It includes anyone who designs, markets, organises

or makes available or implements a reportable arrangement

or anyone who helps with reportable activities and knows or

could reasonably be expected to know that they are doing so.

The guidance, consistent with the approach identified back at

consultation, provides some clarification, identifying two “types”

of intermediary.

The first, “promoters”, actually design, market, organise or make

available or implement a reportable arrangement. The second,

“service providers”, merely provide assistance or advice in

relation to those activities.

The key distinction is that a service provider will not be an

intermediary if they did not know and could not reasonably have

been expected to know that they were involved in a reportable

arrangement. This provides an important safety net for service

providers involved at the periphery of a transaction. An

example given is of a bank providing finance. This is a welcome

clarification: the bank is not expected to make a disclosure if it

does not have sufficient knowledge of the wider arrangements

and, crucially, whether any hallmark is triggered.

Another welcome clarification is that service providers are

not expected to do significant extra due diligence to establish

whether an arrangement is reportable. The bank, in this

example, should do the “normal” due diligence it would do for

the client and transaction in question. Of course, remaining

willfully ignorant will leave the bank on the wrong side of the

“could reasonably be expected to know” test.

Promoters are assumed to understand how the arrangement

works so there is no similar exclusion available to them.

When is there a tax advantage “main benefit”?

A number of the hallmarks only apply if a threshold “main

benefit” test is met (see the table below). This is met where one

of the main benefits that a person might reasonably expect to

derive from an arrangement is a “tax advantage”. The guidance

is clear that HMRC view this as an objective test: what matters

is whether a tax advantage is the main or one of the main

benefits that the person entering into the arrangement might

reasonably be expected to obtain from the arrangement. That

person’s actual motivation in entering into the arrangement

is not relevant. This “main benefit” concept is used in other

UK regimes and is notoriously difficult to apply. The guidance

(following the same approach as taken in respect of a similar

test under DOTAS) views “main benefit” as picking up any

benefit that is not “incidental” or “insubstantial”, a low threshold.

The key to applying this threshold test lies in HMRC’s

interpretation of “tax advantage” and it’s here that the guidance

provides some helpful commentary, in particular noting that

the there be no “tax advantage” if the tax consequences of the

arrangement are in line with the policy intent of the legislation

upon which the arrangement relies. On this basis, HMRC view

products such as ISAs and pensions, designed and intended

to generate a certain beneficial tax outcome, as not meeting

the test unless by reason of being part of a wider arrangement.

Similarly, the guidance gives the example of R&D relief which it

states would not be caught unless the arrangement attempts to

artificially manufacture entitlement.

“Tax advantage” is defined in the regulations as including:

- Relief or increased relief from tax

- Repayment or increased repayment of tax

- Avoidance or reduction of a charge to tax or an assessment to tax

- Deferral of a payment of tax or advancement of a repayment of tax

- Avoidance of an obligation to withhold or account for tax.

“Tax” for these purposes means any tax to which the Directive

applies (i.e. taxes levied by member states other than VAT,

customs duties, excise duties and compulsory social security

contributions).

The hallmarks

This table summarises the hallmarks and, importantly, distinguishes those to which the “main benefit” threshold applies.

| Categories |

Hallmarks |

“main benefit” test? |

Category A

Commercial characteristics seen in marketed tax avoidance schemes

|

Taxpayer or participant under a confidentiality condition in respect of how the arrangements secure a tax advantage. |

✔ |

Intermediary paid by reference to the amount of tax saved or whether the scheme is effective.

|

✔ |

| Standardised documentation and/or structure. |

✔ |

|

Category B

Tax structured arrangements seen in avoidance planning

|

Loss-buying. |

✔ |

| Converting income into capital. |

✔ |

| Circular transactions resulting in the round-tripping of funds with no other primary commercial function. |

✔ |

|

Category C

Cross-border payments, transfers broadly drafted to capture innovative planning but which may pick up many ordinary commercial transactions where there is no main tax benefit. |

Deductible cross-border payment between associated persons… |

|

| |

to a recipient not resident for tax purposes in any jurisdiction. |

|

| to recipient resident in a 0 per cent or near 0 per cent tax jurisdiction. |

✔ |

| to recipient resident in a blacklisted countries. |

|

| which is tax exempt in the recipient’s jurisdiction. |

✔ |

| which benefits from a preferential tax regime in the recipient jurisdiction |

✔ |

| Deductions for depreciation claimed in more than one jurisdiction. |

|

| Double tax relief claimed in more than one jurisdiction in respect of the same income. |

|

| Asset transfer where amount treated as payable is materially different between jurisdictions. |

|

|

Category D

Arrangements which undermine tax reporting under the CRS/transparency.

|

Arrangements which have the effect of undermining reporting requirements under agreements for the automatic exchange of information. |

|

Arrangements which obscure beneficial ownership and involve the use of offshore entities and structures with no real substance.

|

|

|

Category E

Transfer pricing: non-arm’s length or highly uncertain pricing or base erosive transfers. |

Arrangements involving the use of unilateral transfer pricing safe harbour rules. |

|

| Transfers of hard to value intangibles for which no reliable comparables exist where financial projections or assumptions used in valuation are highly uncertain. |

|

| Cross-border transfer of functions/risks/assets projected to result in a more than 50 per cent decrease in EBIT during the next three years. |

|

Key points from the UK guidance

The consultation comments on each category of hallmark.

Category A: the “generic hallmarks”

The “generic hallmarks” (confidentiality, fees based on tax

advantage obtained, use of standardised documentation) are

all subject to the main benefit test. HMRC view the Category

A hallmarks as similar to several hallmarks under DOTAS and

indicated at consultation that they intend to take a similar

approach in interpretation.

Specifically, in respect of standardised documentation, the

guidance notes that under the equivalent DOTAS rules,

arrangements such as ISAs and enterprise investment

schemes are excluded. There is no express exclusion under the

regulations on the basis of HMRC’s view that these kinds of

products are not inherently caught by the main benefit test.

Category B: tax structured arrangements.

Again, these are all subject to the main benefit test. The most

widely discussed of these is Hallmark B2 which captures

arrangements which have the effect of converting income into

capital (or other categories of revenue taxed at a lower rate).

Here the guidance treads a very fine line between situations

where HMRC perceive that a conversion from income to

capital has taken place and those situations where there is a

legitimate commercial choice to be made between different

commercial options. This is an area where further examples

would be welcome although analogies can be drawn. One

example given is of employees given EMI share options as part

of their remuneration where any increase in value in the share

options before exercise could be taxed as a capital gain rather

than income. Whilst the employee could have received salary

income instead, the employer has simply chosen between

viable (normal) commercial options. Other examples pick up

pre-liquidation dividends, company sales where the sale price

includes accumulated earnings, share buybacks and the issue

of securities which qualify as “Excluded Indexed Securities”

under UK law. The addition of steps which are contrived or

outside normal commercial practice would be more likely to

bring the arrangement within the hallmark. A point to note here

is that “conversion” of income into capital does not necessarily

require any pre-existing right to income.

Category C: cross-border payments and double deductions

The guidance provides some useful clarifications in

relation to Hallmark C1 (cross-border payments between

associated persons)

- The “recipient” of a payment will be the person taxable on its

receipt so that, for example, for a partnership, the partners

will be treated as the recipient.

- If the jurisdiction of residence of the recipient of a payment

is not known to the intermediary who is a promoter it is

unlikely to give rise to a reporting obligation. A tax rate is

“almost zero” if it is less than 1 per cent. This applies to

the headline rate of tax, not the effective tax rate a

company faces.

- For payments to recipients in blacklisted countries where

the first step in the arrangement was taken on or after June

25, 2018, but before July 1, 2020, arrangements will only be

reportable under Hallmark C1(b)(ii) where the jurisdiction

appears on the blacklist both on the date the trigger point

is met and on the date that the reporting obligation arises.

This may be helpful given the addition and removal of the

Cayman Islands from the EU blacklist during 2020. For other

arrangements, the list of blacklisted countries should be

examined on the day on which the reporting trigger point

is met.

- When considering whether a payment is tax exempt in

the recipient’s jurisdiction, it is the nature of the payment,

rather than the status of the recipient, that must be exempt:

an exempt body, such as a pension fund will not be

automatically caught.

A number of practitioners had questioned whether Hallmark

C2 (requiring disclosure where depreciation is claimed in more

than one jurisdiction) would lead to an absurd result where

assets are acquired by branches, due to the inclusion and

credit basis on which permanent establishments of UK entities

are taxed. HMRC addresses this: arrangements will not be

reportable where there is a corresponding taxation of profits

from the asset in each jurisdiction where depreciation is also

claimed (subject to any double taxation relief). Whilst this is not

strictly in accordance with the drafting of the directive, which

contains no such carve out, this is a welcome approach from

HMRC as it will enable commercially-motivated transactions to

proceed without the risk of being tainted by disclosure.

Category D: transparency

This hallmark looks at arrangements which have the effect of

undermining CRS reporting or obscuring beneficial ownership.

There is no main benefit test and the test is stated to be an

objective one, so that the intention of the taxpayer is irrelevant.

Having said this, the guidance is clear that arrangements which

merely lead to no report under the CRS being made will not be

undermining or circumventing the CRS provided that outcome

is in line with the policy intentions of the CRS (the example

given is using funds held in a bank account to invest in real

estate, a category of investment specifically excluded from

reporting under the CRS). As is often the case, the examples do

not directly address grey areas. Advising a person to transfer

funds to a jurisdiction which has not implemented CRS, in order

to avoid reporting will, not surprisingly, be caught.

Here again the guidance anticipates that “promoters” will

know whether arrangements undermine or circumvent CRS

whereas a “service provider” may not only have knowledge

of a particular step and may not understand the effect of the

arrangement as a whole, so may not be under an obligation

to report.

The test at Hallmark D2 (arrangements obscuring beneficial

ownership) is whether beneficial owners can reasonably be

identified by relevant tax authorities, including HMRC. This

does not require a public register of beneficial owners but,

where there is a public register, the hallmark will clearly not

apply. Examples of obscuring beneficial ownership include the

use of undisclosed nominee shareholders or of jurisdictions

where there is no requirement to keep, or mechanism to obtain,

information on beneficial ownership. Helpfully, the consultation

states that, as with the OECD’s Mandatory Disclosure Rules

(MDR), institutional investors or entities wholly owned by one or

more institutional investors are outside this hallmark.

Category E: transfer pricing

Responding to questions raised during informal consultation,

HMRC’s guidance confirms that APAs are not unilateral safe

harbours (but rather agreements as to correct pricing) and are

therefore not caught by this hallmark.

Other comments of interest relate to Hallmark E3 (intragroup

cross-border transfers). This hallmark applies where a

cross-border transfer of functions/risks/assets is projected

to result in a more than 50 per cent decrease in EBIT of the

transferor(s) over the next three years. HMRC’s starting point

is to consider this test at company, rather than group level (as

that is how the UK corporation tax regime works) but there

is acknowledgment that many other jurisdictions have tax

consolidation regimes and may take a different approach.

The test looks at projected earnings, not what has actually

happened: if the projections used in reaching a decision not

to report are what a hypothetical informed observer would

consider reasonable, there is no failure to comply whatever

the real-world outcome. HMRC expect relevant entities to be

producing the kind of projections required to apply this test

and would not expect the taxpayer to need to make any special

calculations for DAC 6. There are a number of grey areas

despite some helpful commentary on what will and will not

constitute “cross-border”. Exactly how this would apply (and

whether it would apply) to a number of common transactions,

including an intra-group hive-up of shares, is unclear.

Reporting – what, who and where

The regulations cross-reference the list of reportable information set out in the Directive and clarify that, to be reportable by an

intermediary, information must be in the intermediary’s “knowledge, possession or control”. The guidance expands on this: an

intermediary is not required to trawl through all of its computer systems to try to find all information held in relation to the relevant

taxpayer in order to see if it might be relevant, but the intermediary will be expected to review the documents and information in

relation to the reportable arrangement.

Reportable information

- Identification of taxpayers and intermediaries, including

- Tax residence

- Name, date and place of birth (if an individual)

- Tax Identification Number (TIN)

- Where appropriate, the associated persons of the relevant taxpayer.

- Details of the relevant applicable hallmark(s).

- A summary of the arrangement, including (in abstract terms) a summary of relevant business activities.

- The date on which the first step in implementation was or will be made.

- Details of the relevant local law.

- The value of the cross-border reportable arrangement.

- Identification of relevant taxpayers or any other person in any Member State likely to be affected by the arrangement.

This is a lot of detail. Whoever is making the report will clearly need to devote time to collating information

Where the report should be made

The Directive sets out a hierarchy to determine which member

state a disclosure should be made in and this hierarchy is

cross-referenced to in the draft regulations. The starting point

is that the report should be made in the member state in which

the intermediary is tax resident, failing which, in the location of

a PE connected with the provision of the relevant services and,

where neither apply, in the place of incorporation or, ultimately,

in the member state where the professional association with

which the intermediary is registered is located.

Disclosure only needs to be made once

A transaction is likely to involve a number of intermediaries.

Disclosure only needs to be made once in respect of

arrangements.

This means that no report needs to be made in the UK if:

- The intermediary has made a report in another EU member state

- Another intermediary has made a report setting out (all) the information that the intermediary would have been required to report.

In either case, the intermediary needs to be able to evidence

that the information that it would have been required to report

has been reported, not simply that a report has been made.

The guidance does not provide suggestions as to how the

intermediary achieves this. The expectation is that the filing

of a report will be evidenced by providing the “arrangement

reference number” provided by HMRC or the relevant

competent authority in other member states but provision of

the ARN does not mean that HMRC accepts that the report is

complete or accurate. Determining whether the report made

was comprehensive may be left to the intermediaries to work

out between themselves. An intermediary who has made a

report and subsequently realises it contains inaccuracies is able

to return to it and make amendments.

Documented formal agreement as to who will make the report

should be in place before the actual reporting obligation

commences. It will be beneficial in transactions where

disclosure is thought to be necessary to ensure that all parties

involved are able to cooperate with the reporting process so

that a single, comprehensive report can be submitted. Parties

involved will want to consider rights of review and comment

and will need to ensure that the making of the report will not

breach any contractual terms, including terms of engagement.

It may become common practice in certain types of transaction

to agree contractually who will undertake the reporting

obligation and in what form.

Legal professional privilege

An intermediary unable to report due to legal professional

privilege is required to inform other intermediaries of the fact

and of their reporting obligations. As would be expected, this

does not provide a blanket exclusion from a requirement to

report: legal professional privilege only applies to information

that is legally privileged. The guidance is clear therefore

that lawyers may need to report any information that is not

privileged in nature. The Law Society has published guidance

which sets out its view on when this might be the case and

situations are clearly very limited. In practice, intermediaries

may agree between themselves that reporting will be

undertaken by an intermediary not subject to legal professional

privilege who can make a single report including all the

required information. No doubt the boundaries of this rule will

be tested over time.

Penalties

The penalty regime draws on DOTAS and provides for penalties

in a number of areas. The starting point for failure to report

penalties or a failure to notify of reliance on legal privilege is

a default penalty of £5,000 or, if HMRC consider this too low

(perhaps due to deliberate or repeated failure or where the

failure has serious consequences), the First-tier Tribunal can

impose daily penalties of up to £600 or, as under the DOTAS

regime, if the First-tier Tribunal considers this inadequate it

can impose fines of up to £1 million. There are also penalties of

£5,000 (rising to £10,000 per arrangement for repeated failure)

for failure by a relevant taxpayer to make an annual report in

respect of any arrangement in any year in which it obtains

a tax advantage in respect of the arrangement or to make

three-monthly returns in respect of marketable arrangements.

A penalty will not be imposed where a person has a reasonable

excuse for failure to report. In evaluating this, HMRC will

consider whether a person has “reasonable procedures” in

place to ensure that they are able to meet their obligations

under the regime (and has taken reasonable steps to ensure

those procedures are complied with). As is in the case in other

regimes where this defence is available, what is reasonable

will depend on the circumstances and having procedures

in place will not automatically mean that no penalty is due

(repeated failures, for example, may indicate that procedures

are not adequate and steps should have been taken to address

potential gaps).

There is acknowledgment of the challenges faced by taxpayers

in the period between June 25, 2018 and the publication of

the Regulations and guidance. Where a failure relates to an

arrangement where the first step of implementation predates

the publication of the final Regulations in January 2020 and

the failure was due to a lack of clarity around the obligations or

interpretation of the rules HMRC anticipate some leniency.