Part 1: The building blocks

Revenue stacking refers to the blend of revenue streams available to a project. For the purposes of this article, we have focussed on the following four key components of a revenue-stacking solution:

- A regulated / government-backed revenue support instrument (for the purposes of this article, we have used the UK’s CfD as an example);

- Corporate power purchase agreements;

- Merchant revenues; and

- Power-to-X and energy storage solutions.

Contract for Difference considerations

The UK’s prominence in the global offshore wind market owes much to subsidy regimes such as the CfD and its predecessor, the Renewable Obligation (RO), both of which created regulatory certainty and encouraged investment in the sector. By creating price certainty for both the project’s sponsors and its lenders, the CfD and the RO models addressed a number of early bankability concerns and allowed the fixed bottom offshore wind industry to achieve the scale seen today. On the other hand, such subsidy regimes have removed much of the flexibility from a successful applicant’s revenue strategy by placing limits on any financial upside in times of high power prices and soaring demand. In some jurisdictions, auctions are awarding zero-subsidy contracts. In the UK, some developers have sought to adjust the CfD terms or delay the CfD start date beyond the “target commissioning window”, thereby introducing a merchant nose period and reducing the overall CfD tenor, in light of favourable merchant power markets. For policy reasons however, the UK government has sought to prevent future successful CfD bidders from delaying the contractual CfD start dates solely in order to benefit from high power prices, limiting the ability to take advantage of merchant nose flexibility. This development, coupled with the impact of the renewable energy windfall tax, adds further impetus to adopting a more flexible approach to revenue. In the future, we expect that a greater number of developers will seek a CfD for only a fraction (if any) of the project’s expected installed capacity and will look instead to alternative routes to market.

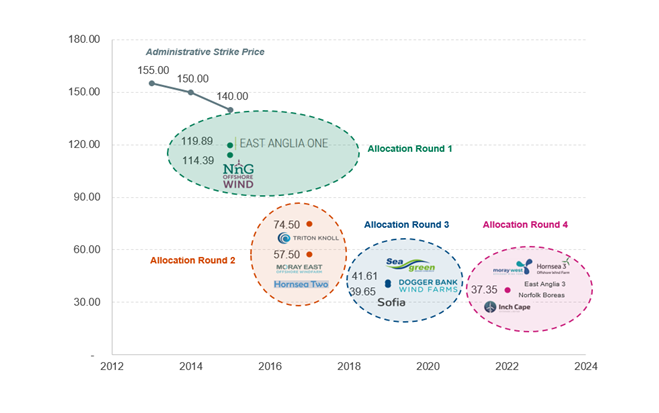

CfD Strike Price Evolution

A total of 7 GW of fixed bottom offshore wind projects were awarded in AR4 compared to 0 GW in AR5.

- The AR5 auction has secured just 3.7GW of new renewable energy – only a third of the total last year and the lowest level since the auction in 2017.

- The auction resulted in a price of £47/MWh (2012 real price) for solar PV (>5 MW) and £52.29/MWh (2012 real price) for onshore wind. This was more than the pricing awarded in AR 4 for solar PV (>5 MW) at £45.99/MWh and onshore wind at £42.47/MWh.

- Whilst offshore wind does not feature in AR5, the government expects the implementation of annual auctions to provide more opportunities for offshore wind developers to participate moving forward. However, auction parameters urgently need to recognize the scale of cost increases on the technical and financing fronts.

Corporate power purchase agreements

CPPAs offer an attractive alternative and/or supplement to the traditional fully-CfD-backed route to market. It is possible that a CPPA can provide a better floor price or fixed price for the generator than is available in the market or under the CfD. Long-term CPPAs are evolving and are now being structured to provide a more flexible hedge against rising electricity costs, with some more sophisticated pricing structures allowing for the re-opening of pricing mechanics if there are material movements in the market. This can also involve different approaches to mitigating inflation risk via contractual mechanics, including inflation caps and floors, as explained below.

Finding a long term solution for electricity sales with sufficient revenue certainty is key to sponsors’ ability to raise limited recourse finance. Whilst a CPPA will provide the offtaker with a hedge against volatile power market prices, the offtaker is also exposed to the risk of prices falling below the fixed price agreed under the CPPA. For this reason, some large corporations may not be willing to agree fixed prices for the 15 to 18 year period typically required to match the standard project finance debt tenors. Long-term CPPAs with a tenor of 10 to 12 years may be more typical and, depending on the financing structure, may be insufficient to align with the financing facility period. A merchant tail will introduce uncertainty of revenue during the final months or years of the loan life, as lenders are asked to take market risk on spot prices in the power market. It may be necessary to introduce sized cash reserve mechanics or require sponsor credit support for such amounts during periods of anticipated lower revenues. Where the debt is repaid on a sculpted amortising basis, with large principal repayments towards the end of the debt tenor, Lenders may look for periodic mandatory prepayment cash sweeps to ensure that the debt is repaid by maturity. As shorter tenor offtake agreements will increase the project’s merchant exposure, it is likely that this approach will impact upon both pricing and debt sizing, and could also lead to “upside sharing” structural mechanics being embedded in the financing, in order to ensure that debt and equity interests, and horizons, remain aligned. Furthermore, as lenders get more comfortable with the commercial contracts, we may start to see renewal risk creeping into debt structures. This could involve shorter dated CPPAs being banked, for a portion of the revenue stack, with a view to renew the contracts during the loan life.

As the popularity of CPPAs continues to grow and corporations come under increased pressure to reduce their Scope 2 emissions whilst hedging against price volatility, it is possible that more attractive terms may be achievable for sponsors during the life of the project. Developers may therefore look to include mechanics in their finance documents to permit the replacement of one or more original offtake agreements where any replacement CPPA is on equal or better terms to the contract being replaced, particularly with respect to key metrics like price, duration and credit worthiness of the counterparty. As alluded to above, short-tenor CPPAs of 3 to 5 years may be attractive to sponsors in the final years of the debt tenor in the event that merchant conditions are not favourable or prices would conflict with the breakeven sensitivities in the financial model.

It is unlikely that there is currently sufficient liquidity in the CPPA market, nor comfort in the banking sector (yet), for CPPAs to completely replace the CfD, but recent experience would indicate that CPPAs will form an important part of the revenue puzzle moving forwards, and that market dynamics, are evolving very quickly.

In a context of high forecast inflation, the value of a robust indexation mechanism in CfD structures, and hence its contribution to bankability, can be fully appreciated. Whilst CPPA offtakers acknowledge these risks, and will undoubtedly continue to accommodate indexation provisions in their CPPAs, we anticipate also that these mechanics may often be caveated with inflation caps. Such caps could represent (subject to base case inflation assumptions, proposed hedging policy, and subsequent demonstrated ability to withstand downsides) a degradation of credit versus the traditional CfD route.

As the universe of potential offtakers for CPPAs grows, we anticipate there will be increasing focus on creditworthiness of offtakers, and the potential sizing of collateral as security to cover the “what if” scenarios. The CPPA market has consisted of large corporations, with clearly identifiable power needs over a long term horizon, and inevitably, credit quality has been strong. As general corporate ESG pressures and incentives increase, we anticipate that the depth and range of the CPPA market will also expand.

CPPAs serve an offtaker’s inherent need for power, whereas CfDs have been used by governments as an instrument to incentivise investment in technologies that would otherwise not have attracted that investment, without such a support mechanism. There are very different reasons behind the use of each, and yet both need to create a secure visible stream of cash flows against which non-recourse financing can be raised. The world has changed since the support mechanisms were initially conceived, and we increasingly see a desire from equity to unlock upside potential from (potentially high(er)) market prices, as opposed to being locked into a competitive strike price for a (long) predetermined period of time. Allied to this general search for yield improvement has been the recent period of high inflation, which has caused dislocation between strike prices (albeit indexed to 2012 figures), fixed early in the development process, and supply contract prices, locked down later. The mismatch between the two has been challenging to manage, as demonstrated by the relative absence of CfD only projects to have so far closed a non-recourse financing on a CfD awarded as part of AR4 in the UK. This is further demonstrated by the recent AR5 results, which has not attracted the same level of interest compared to previous years, as developers assess the trade-off of rising construction costs and the maximum price set by the AR5 auction process. When considering the implementation of various PPAs from a bankability perspective, the different termination mechanics under each CPPA are of vital importance.

CPPA market depth to date has not been for tenors materially exceeding the c. 12 year term, being shorter than the CfD tenor. Increasingly, a layering of multiple revenue sources in any revenue stack is being observed, with different start and end dates resulting in an aggregate contracted/merchant profile which can extend beyond this initial tenor limitation. This stacking and layering, especially when stacking CPPAs alongside CfDs, has so far been used to create bankable projects which accommodate CPPAs with these tenor limitations, and still retain appropriate, from an equity perspective, door to door tenors on the debt. As the market evolves, it is our expectation that shorter dated CPPAs with extension risk may start to be considered in the overall revenue stack.

Importantly, when considering multiple CPPAs within a single project, attention needs to be made with regards to how the offtake strategy for the non-CfD strings’ power output will be sold, as if they are not sold pro-rata across the CPPAs, this creates additional complexity. The commercial replacement risk of each CPPA is also of key importance and a significant bankability consideration.

This article would not be complete without mentioning the relative complexity of aligning multiple CPPA effective dates with an investment decision, especially in a dynamic world of high inflation and volatile energy markets. As a benchmark, the CfD only project template, itself not easy, is much more straightforward – at CfD award date, a developer has certainty on their revenue envelope, and can then proceed to make sure that everything fits within it, and take a subsequent investment decision. When working with multiple offtakers (and potentially also a CfD tranche and/or a merchant element), seeking to lock down supply prices, raise-non recourse financing, and be in a position to take the final investment decision can be challenging, especially as these steps usually need to coincide with each other, This approach may therefore demand some additional flexibility from equity to “bridge” elements of the package falling into place. Consequently, the inclusion of equity bridge loans or back-ended debt may be of increasing consideration.

Merchant exposure

The uncertainties in current power markets have triggered a shift in the approach that banks have taken when considering subsidy-free projects and/or merchant exposure. In addition, strong competition in previous CfD rounds (in particular AR3 and AR4), have forced developers to reassess their revenue strategy and consider merchant exposure with a diverse revenue mix. Increased bank liquidity has pushed lenders to accept an element of merchant risk phased across the debt tenor, to the extent its adequately structured. Merchant risk can be partially mitigated via innovative debt structures and the inclusion of contingency tests in the financing documentation.

- As the market evolves from both an equity and debt perspective, some lenders are more open to accepting a degree of merchant risk and allowing sponsors to benefit from the potential equity upside. Balancing the levels of power sales that are hedged under a fixed price PPA and those that are exposed to merchant power prices will be crucial to structuring a bankable transaction which also provides an attractive return for the project’s sponsors.

- When testing financial ratios, for example in respect of projected debt service cover, consideration will need to be given to the various revenue streams as at each calculation date. The mixture of fixed and variable revenue streams will need to be addressed in the financial covenant package in the loan documentation.

The merchant exposure can be broken into three key phases: (i) the Nose; (ii) the Body and (iii) the Tail.

- Nose: During this period, Lenders have the most visibility of the price expectations. Therefore, there is an option to incorporate a higher level of merchant risk during this period.

- Body: During the body of the debt the merchant level is more restricted. While the merchant upside may be favorable for Sponsors, this needs to be balanced with the wider sensitivity analysis and break-even downside stress tests.

- Tail: Lenders are capable of taking some merchant tail risk but the benefit of the merchant tail would need to be tested with respect to its impact on liquidity and pricing.

Power-to-X and energy storage solutions

The move towards a more integrated energy system is expected to open new power-to-X offtake markets and enable the combination of offshore wind with other solutions (such as large scale storage or green hydrogen production).

Whilst still in the early stages of development, these alternative routes to market could supplement the traditional sale of electricity for end-consumption. Banks will likely require greater comfort around the credit-worthiness of the offtaker, given the nascent and more limited market for green hydrogen production. Further technical analysis will also be required on any battery energy storage systems and/or electrolysers, to assess the projected operating life of such assets as against the debt tenor. Dogger Bank D – a potential fourth phase of the Dogger Bank offshore wind farm in the UK – is reportedly considering using the electricity produced by the project to produce green hydrogen at a facility in the nearby Humber region. Other storage solutions, such as batteries, could also play a key role in supporting the offshore wind sector, with Ørsted recently securing approval for a battery storage project which would serve its 2.9GW Hornsea 3 project in the North Sea. Beyond the UK, there are some further examples projects adopting alternative routes to market. Hollandse Kust North (HKN), an offshore wind project located in Dutch waters, recently generated first power and is another example of a project deploying a novel revenue stack. Approximately 50% of the electricity generated will be sold to Amazon under a CPPA, whilst Shell (which is co-developing HKN with Eneco) will purchase a portion of the remaining output to produce green hydrogen at a nearby facility in the Port of Rotterdam. HKN is also reportedly considering deploying “megawatt scale” battery storage systems. Not only will this give the project access to a separate revenue model, this additional output flexibility will allow generators to better manage output risk and export to the grid during more profitable periods of high demand.