Publication

Global | Publication | September 2022

On 27 July 2022, the UK Financial Conduct Authority (FCA) published its eagerly awaited Policy Statement 22/9 ‘A New Consumer Duty – Feedback to CP21/36 and Final Rules’ (PS22/9), which represents one of the largest pieces of regulatory reform in the UK retail financial services sector for more than a decade. The final rules, which were accompanied by the FCA’s ‘Final non-Handbook Guidance for firms on the Consumer Duty’ (FG22/5), introduces a heightened degree of consumer protection across retail financial services in the UK. Businesses are given until 31 October 2022 to carry out all implementation planning and have their implementation plans scrutinised and signed off by their Boards (or equivalent management body). The next key date is 31 July 2023 at which point businesses must have implemented the rules to apply to all new products and services and all existing products and services that remain on sale or open for renewal.

Implementing and embedding the Consumer Duty will mean significant changes in the ways in which UK financial services businesses operate. The final rules are wide ranging and touch on business-wide governance and oversight arrangements, product governance, individual accountability, distribution arrangements and how businesses interact with retail consumers on a day-to-day basis.

It is important that you familiarise yourself with this new Consumer Duty, and contemplate any prospective impact that it may have on your operations should Australian regulators consider adopting a similar framework in the future, or how changes to the UK system may be imported to the current regulatory regime in Australia. To assist you in this process, this article summarises the key components of the new Consumer Duty and compares it with existing Australian regulatory mechanisms. The question is: will Australia follow suit?

The Consumer Duty aspires to set a higher level of consumer protection by shifting the focus from profit to consumer benefit. By doing so, businesses will be challenged to reorient themselves to deliver good outcomes for their customers. This reorientation is effected through four broad outcomes, which cut across the UK financial services market:

In doing so, the Consumer Duty will impose a requirement on firms to undertake a significant cultural and behavioural shift to ensure that businesses put consumers first and take account of behavioural biases and characteristics of vulnerability.2 The Consumer Duty applies to a broad basis of financial services providers, both retail and wholesale. Importantly, this includes all firms that can determine or materially influence retail consumer outcomes, regardless of where they sit in the distribution chain. Products and services that are not designed for retail consumers are not in scope of the Consumer Duty, where they are only marketed and approved for distribution to non-retail consumers, and are not provided to another firm under an arrangement between them as part of a distribution chain for a retail product or service.3

In the article that follows, we unpack some of the key takeaways and obligations under the Consumer Duty before exploring the extent to which a similar duty could be on the horizon here in Australia.

The introduction of the new Consumer Duty is driven by the need to strengthen consumer protection in retail financial markets, within a framework which incentivises vigorous competition in the interests of consumers, and within which consumers are empowered to make informed choices about financial products and services.4

The Consumer Principle does not change the nature of a firm’s relationship with its consumers. For example, it does not create a fiduciary relationship where one would not otherwise exist, nor require a firm to carry out any regulated activity (for example, provide advice) where it would not otherwise have done so.

The FCA conducted an extensive consultation process on the proposed Consumer Duty in two consultation papers (CP21/13 – Consultation Paper released May 2021; CP21/36 – Draft Rules and Guidance released December 2021). The Policy Statement and final rules were published on 27 July 2022, with an implementation timetable for businesses to meet, requiring that:

The FCA has indicated that the Consumer Duty will be fundamental to its outcome-focused regulatory approach, which it believes can be applied more easily to technological updates and market developments than prescriptive rules in order to address consumer harm.5 Examples of consumer harms identified by the FCA include:

By embedding the Consumer Duty into its authorisation, supervision and enforcement approach, it will enable the FCA to increasingly focus on the outcomes that consumers experience. The FCA has stated that this, combined with its more “data-led” approach, should enable it to intervene more quickly than it has done previously where it identifies practices that have an adverse impact on customer outcomes and more assertively before those practices become entrenched as market norms.6

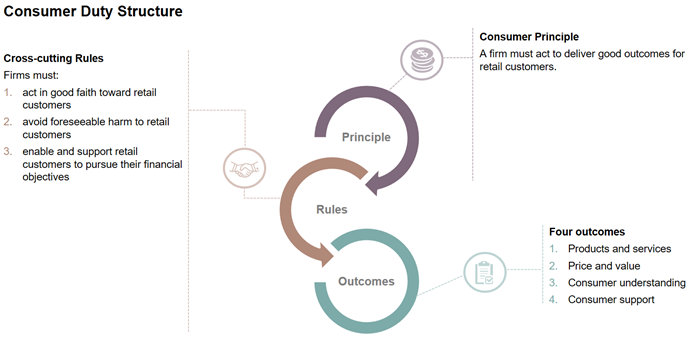

The diagram below captures the key elements of the new Consumer Duty:

The Consumer Principle (Principle 12) reflects the overall standards of behaviour the FCA wants from firms, and is developed by the other elements of the Consumer Duty.7

Principle 12 sets out FCA’s expectations of firm conduct – to think more about consumer outcomes and put consumers’ interests at the heart of their activities. It is expected to prompt firms to ask themselves questions such as whether they are treating consumers as they would expect to be treated in their circumstances.8

Principle 12 focuses on consumer outcomes, and requires businesses to:

The underlying purpose of the Consumer Principle is not to compel firms to protect individual customers from poor outcomes nor is it that consumers will always end up with a good outcome. Further, it also does not impose an open-ended duty to protect consumers from all potential harms. For example, firms, insofar as they have complied with the Consumer Duty, are not expected to protect consumers from risks that are inherent in a product’s structure or design, such as investment risks.

The Consumer Principle will be underpinned by a set of ‘cross-cutting’ rules which set out how firms should act to deliver good outcomes for retail customers and the standard of conduct that the FCA expects under Principle 12. They require firms to:

The cross-cutting rules are intended to work together as a package, meaning that poor conduct may result in a breach of one or more cross-cutting rule.

Compliance with the cross-cutting rules is likely to require a consideration of how the new Consumer Duty interacts with existing regulatory duties. Firms may use existing compliance mechanisms as a springboard to establish an appropriate compliance framework. However, given the broader nature and the heightened requirements under the Consumer Duty, compliance with existing rules may not be sufficient in all circumstances to prove compliance with all aspects of the new Consumer Duty.12

The FCA has confirmed that the Consumer Duty applies to all businesses that have a material influence over, or determine, retail consumer outcomes. For example, it applies to businesses that can influence material aspects of, or determine:

Whether a material influence exists depends on the actual circumstances. For example, a material influence would not include a firm whose role is limited to:

The extent of a firm’s obligations under the Consumer Duty will depend on its role and the reach of its influence over retail consumer outcomes, even where the end consumers in the distribution chain is not a direct client of the business concerned.15

The Four Outcomes represent the key elements of the firm-customer relationship, and build on the Consumer Principle and the cross-cutting rules:

To be able to deliver good consumer outcomes, all products and services for consumers are expected to be fit for purpose, i.e. designed to meet the needs, characteristics and objectives of a target group of consumers and distributed in an appropriate manner. It should be noted that a firm can be both a manufacturer and a distributor.

The FCA is proposing to impose different obligations for firms, depending on their role in the distribution chain, as tabulated below.

| Role | Who is captured | Non-exhaustive list of obligations |

| Manufacturers |

A firm which:

|

The key obligations include the requirements to:

|

| Distributors | A firm which offers, sells, recommends, advises on, arranges, deals, proposes or provides a product or service. |

The obligations include:

|

The FCA wants all consumers to receive fair value. In the FCA’s view, value is about more than just price. It wants businesses to assess their products and services in their totality to ensure that the price a customer has paid for a product or service is reasonable compared to the overall benefit the consumer obtains. The FCA makes clear that low prices do not always mean fair value. Importantly, businesses must make an assessment of value when designing products or services and prior to offering them to consumers. They must also ensure that the price represents fair value for a foreseeable period of time and throughout the lifespan of those products or services. Appropriate action must be taken where a firm identifies that a product or service does not provide fair value.

In order to assess whether a product or service provides value, the FCA expects businesses to consider at least the following:

If products and/or services are sold together as part of a package, it is important to ensure that fair value attaches to each component product or service as well as the overall package.

The FCA wants consumers to be provided with the necessary information at an appropriate time, with the information presented in a manner to facilitate their understanding.

Principle 7 requires businesses to communicate information in a way which is clear, fair and not misleading. Building on Principle 7, the Consumer Understanding principle extends the requirement for firms to:

An important question the FCA is encouraging all businesses to ask themselves in the context of this outcome is ‘whether they are applying the same standards to ensure their communications are delivering good consumer outcomes as they do to ensure their communications help to generate sales and revenue’.18

The Customer Support rules are the overarching requirements set out by the FCA in terms of the level of support that businesses are expected to provide to consumers for the duration of their relationship with the firm. Firms should provide a level of consumer service enabling consumers to realise the benefits of the purchased products and services and ensure that they feel supported to pursue their financial objectives.

The rules under the Consumer Support outcome and the Consumer Understanding outcome are closely related. In particular, the FCA states that ‘[u]nder the consumer understanding outcome businesses should communicate with customers in a way that equips them to make effective, timely and properly informed decisions. Under the consumer support outcome businesses should enable customers to act on these decisions without facing unreasonable barriers’.19 Businesses should always remind themselves of their obligations under both outcomes in all consumer interactions.

An important question the FCA is encouraging all businesses to ask themselves in the context of this outcome is ‘whether they are applying the same consumer support standards to deliver good consumer outcomes as they do to help generate sales and revenue’.20

While there are examples of regulatory mechanisms which are comparable to aspects of the Consumer Duty and its effect on financial institutions and the wealth business, the Australian regulatory landscape does not yet include a holistic Consumer Duty regime.

In response to the Banking Royal Commission and the resulting increase in active regulation of the financial services industry, various measures focusing on consumer outcomes have been introduced. The current Australian framework imposes a range of obligations on regulated entities through various instruments. In addition to the general duty of financial services and credit licensees to act efficiently, honestly and fairly, this includes the following key obligations:

1. Mortgage Brokers Best Interests Duty (RG 273) which requires mortgage brokers to:21

2. Financial Advisers Best Interests Duty (RG 175),24 which requires advice providers to:

3. Design and Distribution Obligations (RG 274), which imposes requirements on:

The introduction of the Consumer Duty in the UK is indicative of a growing appetite globally by regulators to intervene and impose minimum requirements protecting retail consumers regardless of their sophistication. The Consumer Duty will set higher expectations for the standard of care firms give consumers than have previously existed and is compatible with, but does not replace, existing rules within the FCA Handbook.

The question for financial firms in Australia is whether they should expect the government to introduce an Australian version of the Consumer Duty. It may be worthwhile for Australian financial firms to proactively evaluate their business practices to determine what work will be required to allow them to comply with a consumer duty similar to that in the UK. At the very least, this exercise would also test compliance with the Australian obligations we identified above, whether or not a consumer duty is ultimately introduced.

If you would like to know more about the new Consumer Duty, please click through to:

Should any of the above raise any concerns or queries as to their application to your circumstances, our global financial services regulatory team and risk advisory specialists are available to assist.

PS22/9: A new Consumer Duty (fca.org.uk), 5.14 “Enabling customers to pursue their financial objectives”.

PS22/9: A new Consumer Duty (fca.org.uk), 2.20 "Impacts for the wholesale sector.

PS22/9 at 1.3 and 5.14.

PS29/9 at 1.7.

PS22/9 at 14.2.

FG22/5 at 1.3.

FG22/5 at 4.3 and 4.4.

PS22/9, Annex B, at [2A.2.2].

PS22/9, Annex B, at [2A.2.6], [2A.2.9].

PS22/9, Annex B, at [2A.2.20].

CP 21/36, Appendix 2 at [5.46-49].

FG22/5 at 2.13.

FG22/5 at 2.15.

FG22/5 at 2.16.

PS22/9 at 2A.4.18R.

PS22/9 at 2A.3.14 – 2A.3.20.

PS22/9 at 8.11.

FG22/5 at 9.4.

FG22/5 at 9.5.

For more information see: Division 2, Part 3.5A, National Consumer Credit Protection Act 2009 (Cth) (the NCCP Act).

Sections 158LA and 158LE of the NCCP Act.

Sections 158LB and 158LF of the NCCP Act.

Pt 7.7 and Div 2 of Pt 7.7A of the Corporations Act 2001 (Cth).

For an overview of the Best Interests Duty and Related Obligations; see Regulatory Guide RG 175: Licensing Financial Product Advisers – conduct and disclosure at p 64 [Table 5].

Section 961J of the Corporations Act 2001 (Cth).

For further details, please refer to Part 7.8A, Corporations Act 2001 (Cth).

Publication

Marta Giner Asins and Arnaud Sanz of our Paris office are the authors of a chapter on product denigration that has been published in the third edition of the Global Competition Review’s The Guide to Life Sciences.

Publication

Miranda Cole, Julien Haverals and Emma Clarke of our Brussels/ London offices are the authors of a chapter on procedural issues in merger control that has been published in the third edition of the Global Competition Review’s The Guide to Life Sciences. This covers a number of significant procedural developments that have affected merger review of life sciences transactions.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2023