Publication

Global rules on foreign direct investment (FDI)

Cross-border acquisitions and investments increasingly trigger foreign direct investment (FDI) screening requirements.

Global | Publication | October 2017

VAT is being introduced in the UAE from January 1, 2018 as part of the wider introduction of VAT by members of the Gulf Cooperative Council (GCC). It is expected to raise significant revenues: AED20 billion in the second year (approximately $5.5 billion). The head of the Federal Tax Authority (FTA) has confirmed recently that online registration will open by the end of September1. The basic VAT law Federal Decree Law No. (8) of 2017 on Value Added Tax (the Decree) was published on August 27. The underlying regulations (providing detail on the operation of the new VAT system) are expected in the fourth quarter of this year. Businesses that are required to register must have done so by January 1, 2018 and it is possible that regulations may specify an earlier date to avoid a last-minute rush on registration.

The GCC member states signed a Framework Agreement for the introduction of VAT back in 2016. This set out the basic principles for GCC VAT allowing some scope for implementation to vary between members. The UAE Ministry of Finance (MoF) has released some details of how it will implement the regime. This, taken alongside the Decree, enables us to see, in broad outline, how GCC VAT is expected to operate.

The introduction of VAT presents some obvious systems and compliance challenges in terms of invoicing and accounting for the new tax, but it is also essential for businesses to be aware of and prepare for the effect of VAT on contract documentation, group structuring/ restructuring and mergers and acquisitions (M&A).

Some risk areas are sector specific, others apply to specific transaction types. The basic Framework for GCC VAT does not replicate all the characteristics which have given rise to complexities in the EU VAT system, but the broad concepts are aligned which means that we can draw to a significant extent on experience of the operation of VAT in the EU in order to identify risks and those areas where pre-emptive action can be taken.

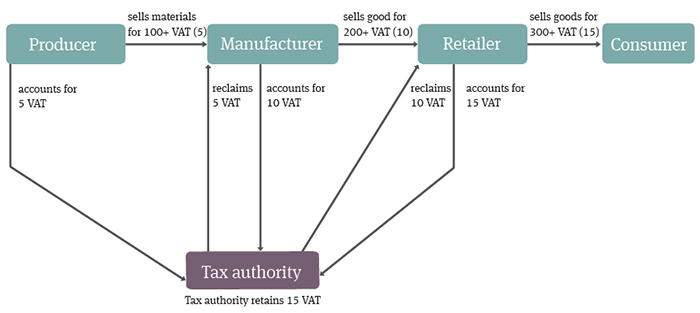

VAT is a tax on consumption of goods and services supplied by “taxable persons” (persons carrying out an economic activity which requires them to be VAT registered). It is an “indirect tax”, meaning that it is, in most cases, collected and accounted for by the supplier on behalf of the tax authority. A key feature is that it is designed to be borne by the ultimate consumer but is charged on each transaction in a supply chain. To achieve this it allows for recovery of VAT incurred on supplies received where those supplies are used to make further taxable supplies.

By way of example, taking the five per cent GCC VAT rate:

For a “taxable business” making fully “taxable supplies” VAT incurred should be fully recoverable and should not represent any real cost to the business. However, the basic concept of a tax borne by the ultimate consumer is deceptively simple and, in the EU, implementing legislation has given rise to a vast amount of litigation. A large amount of this complexity arises from the distinction between “fully taxable”, “zero rated” and “exempt” supplies. The distinction is particularly important due to its effect on the ability of a supplier to recover VAT incurred on supplies made to it. A “zero-rated” supply is a “taxable supply”, but a VAT exempt supply is not and impacts the ability to recover VAT incurred on supplies received. VAT is a real cost for businesses making exempt supplies.

VAT impacts most transactions. VAT regimes give rise to difficult and complex issues simply in terms of determining the basic VAT liability. There are then specific structuring and transaction concerns.

Businesses making or receiving cross-border supplies or making supplies of financial services or land will want to pay particular attention to the detail of the draft legislation released by each GCC member state. There will also be important sector-specific developments to follow in other areas including aviation, oil and gas and construction.

As a general matter, where a contact is silent on VAT, the price will be deemed to be VAT inclusive. The MoF has indicated that a transitional regime will apply, however, to existing contracts; this will mean that a supplier can make an additional charge for VAT where part of a supply under an existing contract is made on or after January 1, 2018, provided that the customer is able to recover it. Detail is expected in the regulations. Contracts which will continue in effect after January 1, 2018 should be reviewed and, if necessary, renegotiated to ensure that they work appropriately for VAT.

Online registration opened on September 17.

Publication

Cross-border acquisitions and investments increasingly trigger foreign direct investment (FDI) screening requirements.

Subscribe and stay up to date with the latest legal news, information and events . . .

© Norton Rose Fulbright LLP 2023